Continue with onX Maps

Continue with onX Maps Sign in with Facebook

Sign in with Facebook

When wealthy adventurers take huge risks, who should pay for rescue attempts?

|

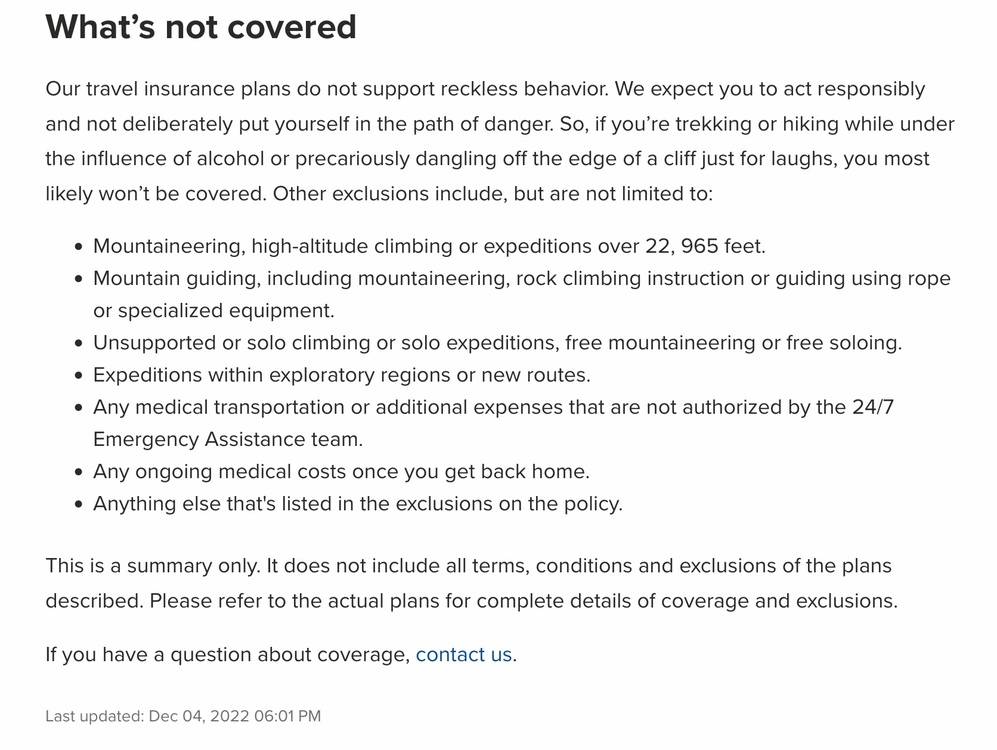

Long Rangerwrote: It seems like the vast majority of climbing would be covered. The rock climbing exclusion reads as though in pertains to those engaged in the act of guiding, not the act of following a guide. |

|

Lion Forestwrote: I wouldn’t bet on it without checking with that company though. I’ve had a claim denied because I was wearing climbing shoes. Rock shoes fell into a “specialized equipment” category, as did “backpacking boots” and “footwear designed to be worn in the water, including snorkeling fins and wading boots.” It was all in the fine print but there were a lot of phrases (“specialized equipment”) that weren’t defined in that section, and sometimes the definitions had caveats like “including but not limited to…” just like the policy above. |

|

|

F Wheelerwrote: Never bet on reading a contract, that's what attorneys are for. |

|

|

Lion Forestwrote: Yup. For context, I was climbing a rock wall on a cruise ship, wearing the provided shoes, and the claim was with the travel insurance company the cruise company had recommended, soooo…I figured I’d be covered. Lesson learned. |

|

|

F Wheelerwrote: Yeah, those recommended companies/plans almost always suck. FWIW, I've had good luck with (albeit non-injury claims) with Travelex. |

|

|

Cherokee Nuneswrote: Yeah, for sure. This obviously explains why the government has totally banned all hiking, climbing, SCUBA, whitewater rafting, skiing, boating, swimming in bodies of water deeper than 6 inches, etc. And guns, too! |

|

|

I've seen numerous trails closed "too dangerous" this spring alone. Gotta register that boat. Yawn. I could go on. Got anything else? |

|

|

Wealthy adventurers!!! Ok, but what percentage of search and rescue do they really amount to? I'm thinking this is just invention of a reason to be angry at other people. |

|

|

Cherokee Nuneswrote: Registering a vehicle is now the same as banning something? LOL. Seriously, if what you propose is true, Mt. Whitney would have been off-limits starting decades ago. Southern California beaches would be closed every time there's a big swell. Denali, well, just forget about that... |

|

|

Lion Forestwrote: I'm not quite so sure, as this isn't the actual policy, just a summary of what to expect on the actual policy. When you hide the actual policy through so many flaming hoops, what does that tell you? I really don't like the part of this summary that says, "call the number before you basically do anything". That works great, except when you can't get a signal (or a million other things go wrong). But again, just purely as an example. No "cheap" insurance for a climbing trip is worth it. I think there's insurance policies that COULD be worth it, but you'll be paying for the privilege - and you still need to do your homework. In most cases - I just don't know if it's honestly, 100% worth it? |

|

|

Devin Hanes wrote: Nah, I don’t really care. |

|

|

Devin Hanes wrote: Yes. What’s your point? |

|

|

Marc801 Cwrote: This is true. I once was the first person on scene at a HORRIBLE mountain biking crash. I saw him wipe out and when I ran to the guy's side he was face down in the dirt having a seizure. Based on the violence and nature of the crash I was pretty sure his neck was also broken. I laid beside him in the dirt and kept him as safe and calm as possible while I called 911. Local paramedics came and transported him to the hospital on a backboard with neck brace where, in fact, it turned out he had a fractured but not completely severed cervical vertebrae from the crash. I'd left a note in his bike pack with my name, number and, "You probably won't remember me but I witnessed your entire crash and called 911 for you. If you want to know what happened call me at _______." |

|

|

Andrew Ricewrote: I had a good friend in Canada whose life partner was killed by a grizzly. They owned a condo in town with a mortgage. Working class. One child, a daughter about 5 or so. At most real estate closings in N. America today, one of the many items a lawyer or title company tries to sell to homebuyers at the table, because they earn a commission for selling ad on's, is a mortgage life insurance policy. Mortgage life policies pay off the balance of a mortgage if two folks mortgage a home together. A popular product assuming if a two income household loses one of those incomes, they could end up not being able to perform on the mortgage. Of course there was tons of media coverage regarding this incident, local and national, as there always is when wildlife kills a human. This event happened in town via a trail run. There were three female runners together. My friends partner climbed a tree and the young male grizzly knocked her out of the tree and killed her. When my friend got around to processing his mortgage life insurance claim, they sent a denial letter. Their excuse was that by her climbing the tree, it was considered reckless behavior on her part. I assisted him in writing a simple one page letter that gave the insurance company two weeks to change their mind before employing a press release regarding the situation. They paid the policy promptly. The moral of the story, yes, you only get what you fight for in this capitalistic world. It is always the way it has been. If you want to pay insurance premiums, simply know, you will still automatically have to fight for just about any claim. |

|

|

Dow Williamswrote: That's awesome, Dow. I guess the insurance company thought it would have been safer to just lie down for the charging grizzly? Good for you sticking up for your friend. |

|

|

Andrew Ricewrote: It's all just lawyer tactics. A defense will do anything in their power to get the best outcome for their client. Insurance companies just know they're the ones who write the rules and also the ones who may need to follow them. But they can make those rules favor themselves and be opaque to anyone other than themselves and an actual expert. It's disgusting that they needed to have their reputation of all things tarnished for them to do the actual correct human thing. Man I'm salty. |

|

|

Devin Hanes wrote: I don’t work in the insurance industry. |

|

|

Devin Hanes wrote: |

|

|

Tradiban wrote: No you're not. You're going to sit and wait on your couch until your max post limit resets and will be right back here trolling. |

|

|

Chad Millerwrote: Going Sunday actually, how bout you? |